Today the Fraunhofer Institute for Solar Energy Systems ISE presented the data on net public electricity generation for the first half of 2023 from the Energy-Charts data platform. Renewable generation, with a share of 57.7 percent of the net electricity generation for public power supply, that is, the electricity mix that comes out of the socket, was significantly higher than the first half of 2022 (51.8 percent). The share of renewable energies in electricity consumption was 55.5 percent. With the first six months of 2023, solar and wind power plants fed a total of 97 terawatt-hours (TWh) into the public grid, compared to 99 TWh in the first half of 2022. The electricity production from lignite was down 21 percent, hard coal was down 23 percent, natural gas was down 4 percent, and nuclear declined by 57 percent, compared to 2022 values.

The first half of 2023 saw a normalization of energy prices, with natural gas prices and electricity exchange prices returning to pre-Ukraine war levels but still above 2021 prices. The impact of the nuclear phase-out, with the shutdown of the last nuclear power plants Isar2, Emsland and Neckarwestheim2 in April 2023, has been absorbed well. Factors such as increasing production from renewable sources, weather and higher production in neighboring European countries are significantly stronger than the effect of shutting down the three nuclear plants. The approximately 30 TWh from the reactors was offset by reduced exports, increased imports, and the addition of solar and wind capacity.

Load was 234 TWh in the first half of the year (H1 2022: 250 TWh), continuing the declining trend. Electricity production decreased from 252 TWh to 225 TWh compared to the first half of 2022. Exports of electricity to France decreased after the French nuclear reactors came back online. Exports to Austria and Switzerland decreased due to the countries' higher in-house generation and lower consumption. In the first quarter of 2023, more electricity than usual was imported because electricity prices in neighboring countries were favorable.

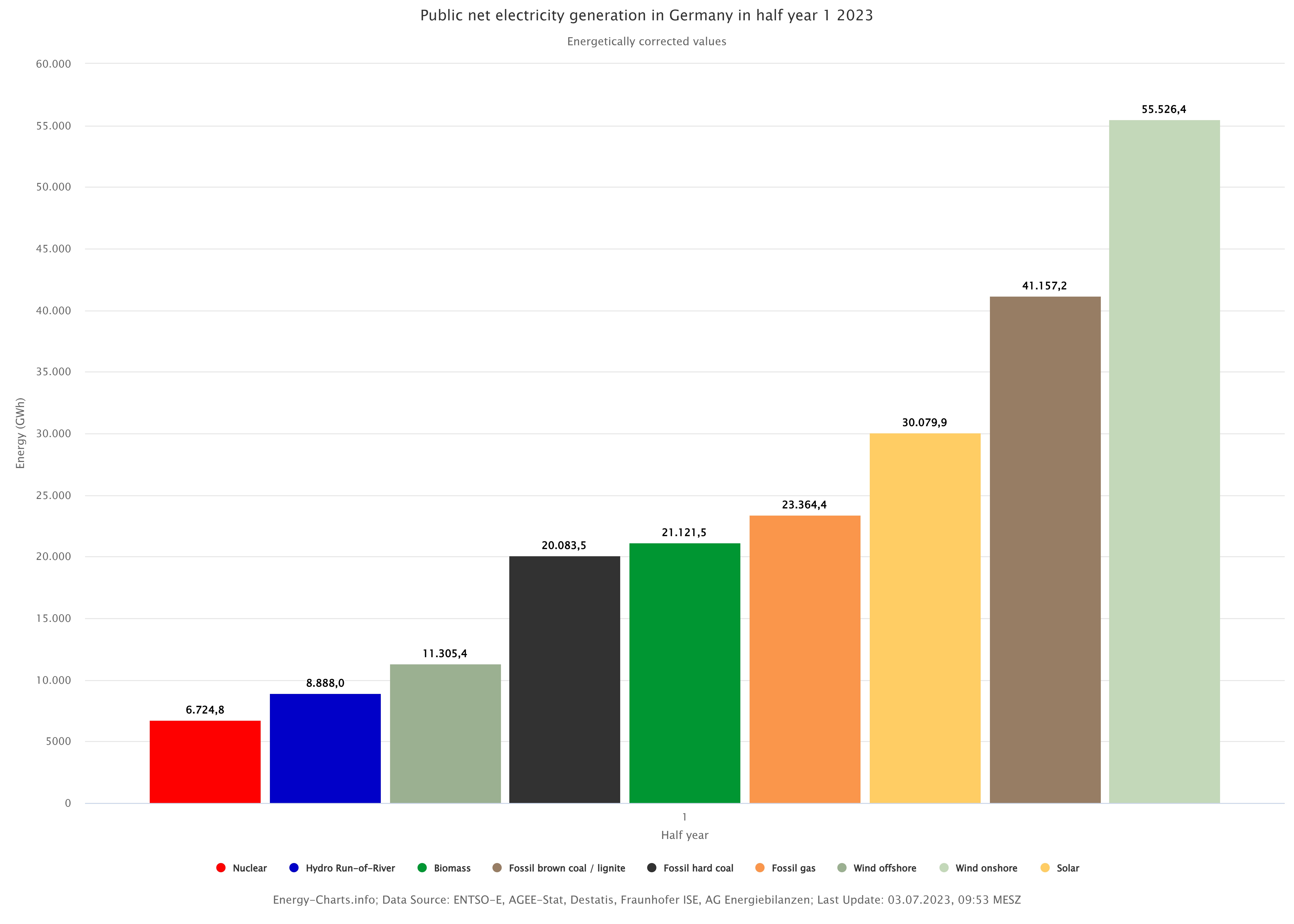

Wind energy was by far the most important renewable energy source. Wind turbines produced 67 TWh in the first half of 2023, down slightly from the first half of 2022 (about 68 TWh). February was a weak wind month, lowering the overall result. Photovoltaic systems fed approximately 30 TWh into the public grid in the first half of the year, a slight decrease from the previous year's 31 TWh, for which the weak month of March was mainly responsible. Solar power plants thus accounted for 12.5 percent of net public power generation. On May 4, they set a record: for the first time, solar plants in Germany fed more than 40 GW of power into the grid. With about 15 TWh of solar and wind power generation, June set a new monthly record for a June month. Hydropower produced 9.3 TWh in the first half of the year, up from 8.2 TWh a year earlier. Biomass power generation was on par with last year at 21 TWh.

In total, solar, wind, hydro, and biomass renewables produced about 130 TWh in the first half of 2023, down slightly from 131 TWh a year earlier. The share of net public electricity generation, i.e., the mix of electricity that actually comes out of the socket, was about 57.7 percent, well above the first half of 2022 (51.8 percent).

The last three nuclear power plants generated 6.7 TWh until their shutdown on April 15. In the first half of 2022, the figure was 15.8 TWh.

Coal-fired power generation also fell: Lignite-fired power plants generated about 41.2 TWh, a sharp decline of 21 percent from 2022 (52.1 TWh). Net production from coal-fired power plants also decreased by 23 percent, from 26.2 TWh in 2022 down to 20.1 TWh in 2023. Electricity generation from natural gas decreased only slightly from 24.3 TWh to 23.4 TWh. In addition to gas-fired power plants for the public power supply, gas-fired plants in the mining and manufacturing sectors also supply the industrial own consumption. These approximately produced an additional 24 TWh for industrial captive use.

The volume-weighted average electricity price in the day-ahead auction was 100.54 euros/MWh. This is a significant decrease compared to the first half of 2022 with 181.28 Euro/MWh.

The average price for natural gas in the first half of 2023 was 45.29 euros/MWh. In the first half of 2022, the price was 99.84 euros/MWh.

The average CO₂ certificate price per metric ton of CO₂ in Germany has risen to 86.97 euros, double the 2021 amount, while the volume-weighted average electricity price in the day-ahead auction was 100.37 euros/MWh.

The addition of photovoltaic capacity is currently within the target corridor of the German climate protection goals: From January to May alone, 5 GW was added, which would meet the target of 9 GW in 2023. Wind expansion, on the other hand, is not on track: By the end of May, 1 GW had been installed onshore and 0.23 GW offshore, indicating that the target of 4 GW will not be reached.

There has been great movement in the field of battery storage. In the first half of 2023, 1.7 GW of storage capacity with a storage capacity of 2.4 GWh was added, so that 5.6 GW of capacity with 8.3 GWh of capacity is now installed in Germany. By the end of the year, this capacity will increase to 10 to 11 GWh.